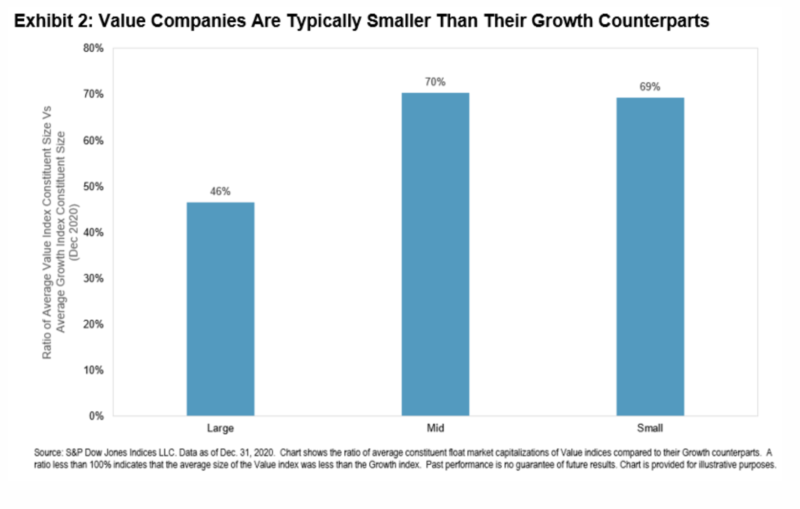

Both value stocks and smaller companies have outperformed so far this year. But sincevalue-oriented companies are typically smaller than their growth counterparts, is the recent resurgence of the value premium simply a consequence of its smaller size exposure? HAMISH PRESTON from S&P Dow Jones Indices takes a closer look.

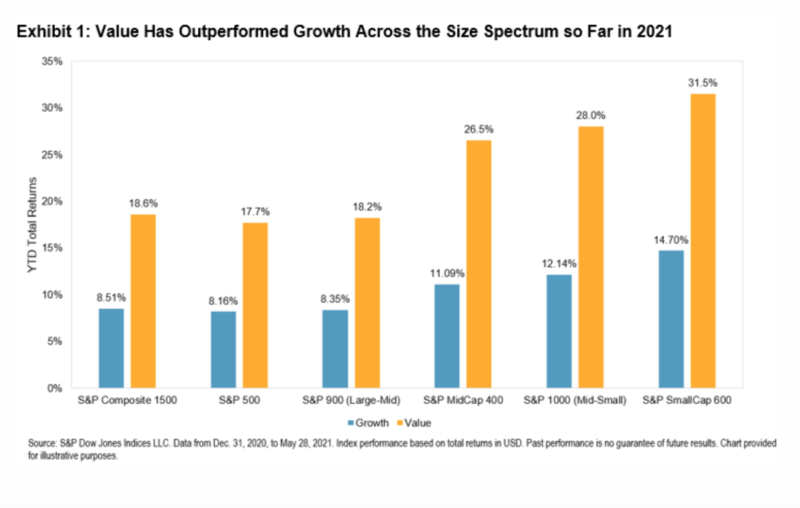

After more than a decade of underperformance, and in stark contrast to Growth’s dominance for much of 2020, Value has made an impressive comeback so far in 2021, outperforming Growth around the world, including across the size spectrum in the U.S. In fact, Value’s YTD outperformance against Growth in mid and small caps is the largest it’s ever been as of the end of May, while the S&P 500 Value’s 9.5% YTD outperformance is the second highest in its history through the first five months of a year.

Smaller companies have also outperformed so far this year, which helps to explain why Equal Weight indices, with their smaller size tilt, have outperformed their cap-weighted parents. But the outperformance of smaller size raises an obvious question: sincevalue-oriented companies are typically smaller than their growth counterparts (see Exhibit 2), is Value’s recent resurgence simply a consequence of its smaller size exposure?

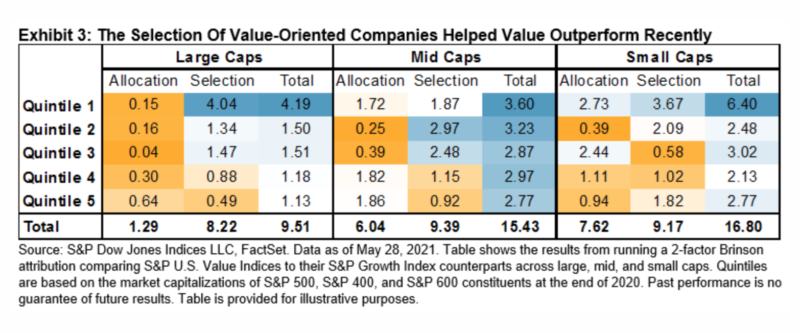

In order to analyse the role of size in explaining Value’s recent returns, S&P 500, S&P MidCap 400, and S&P SmallCap 600 constituents are divided into quintiles based on their market capitalisations at the end of 2020. Quintile 1 contains the largest 20% of stocks (by stock count) in each size segment, while Quintile 5 contains the smallest stocks.

Exhibit 3 shows the proportion of Value’s YTD excess returns that are attributed to selection and allocation effects across the different quintiles in large, mid, and small caps. If size was the only determinant of Value’s relative returns, the allocation effect would equal the total effect: there would be no impact from selecting value-oriented stocks. However, the choice of value-oriented constituents (selection effect) was typically more important than allocations to different size quintiles (allocation effect) and the selection effect accounted for the majority of Value’s YTD outperformance.

As a result, Value’s recent resurgence has been driven by the outperformance of more value-oriented companies rather than by their smaller size. And while we will have to wait and see what happens across the style box in the coming months, many investors may be enjoying riding the value wave for the first time in a few years.