It can't be said often enough that, for all investors, global diversification is critical. And yet, the world over, investors have an unhealthy bias towards their own stock market. This is very much the case in Britain, where investors are paying a price in terms of risk and returns for their predilection for UK equities. If there’s one overseas market that all UK investors should have exposure to it’s the United States, as SHERFA ISSIFU from S&P Dow Jones Indices explains.

Our recent paper Why Does the S&P 500® Matter to the U.K.? argues that the S&P 500 presents an opportunity for U.K. investors to diversify their revenue exposure and sector weights across geographies. Since British investors typically suffer from a substantial home bias, such diversification presents an opportunity to improve the risk/return profile of a domestic equity allocation.

U.K. companies and U.K. investors are exposed to the same set of domestic macroeconomic conditions. When a large proportion of a company’s revenue is reliant on its domestic customer base and an investor in turn overweights his allocation to U.K. equity, it creates a domestic feedback loop. This means that positive and negative shocks in the U.K. are amplified for a local investor who is not properly diversified.

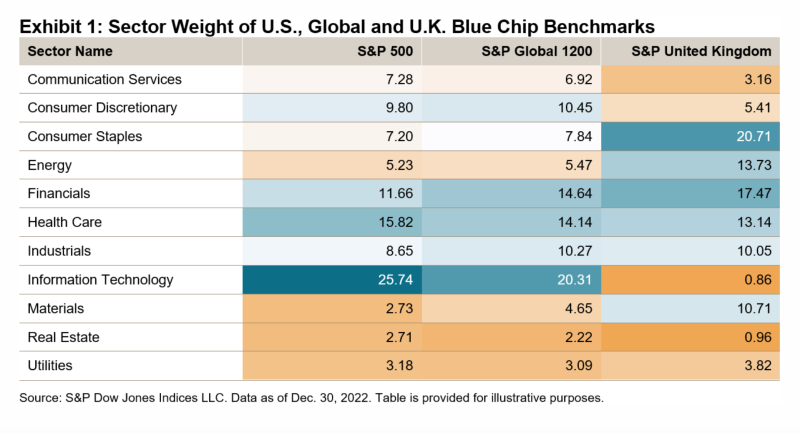

Moreover, the U.K. has more significant over- and underweights than the S&P 500 relative to a global benchmark. Exhibit 1 compares the sector weights of the S&P 500 and S&P United Kingdom versus the S&P Global 1200. The S&P United Kingdom had larger sector weights than the S&P Global 1200 in Consumer Staples, Energy and Materials, and a far lower weight in Information Technology. On the other hand, the S&P 500 was overweight IT and Communication Services. Hence, incorporating U.S. equities could help a U.K. investor alleviate domestic sector biases by providing exposure to different sectors.

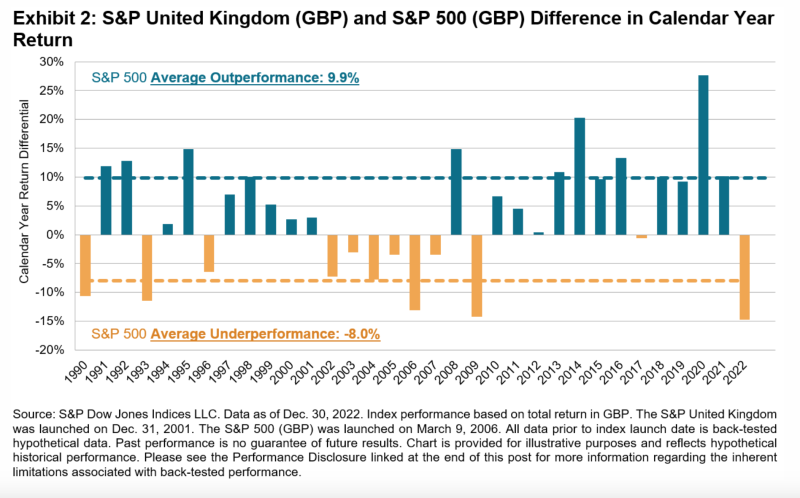

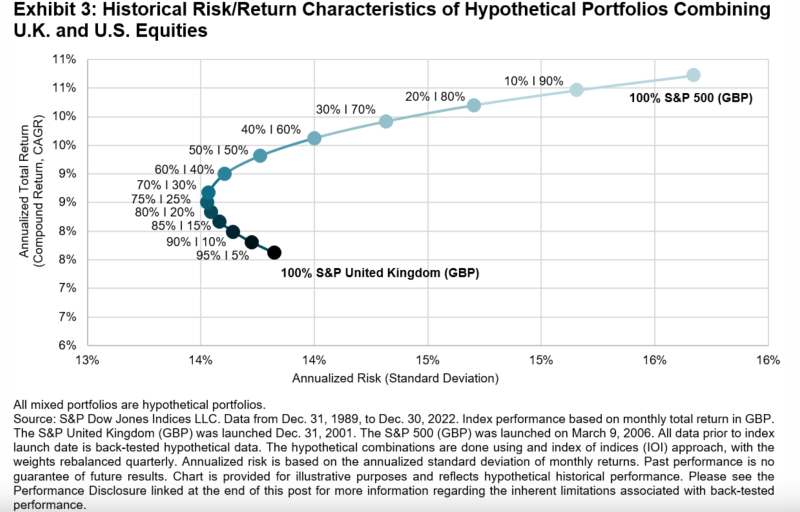

From a performance perspective, U.S. large caps have outperformed their U.K. counterparts most of the time and by a larger magnitude when they do. Over the past 33 calendar years, the S&P 500 has outperformed the S&P United Kingdom two-thirds of the time, as shown in Exhibit 2. In the years when the S&P 500 outperformed it did so by a higher margin on average, at 9.9%, compared to the U.K.’s 8%. This has meant combining the S&P 500 and the S&P United Kingdom (as shown in Exhibit 3) has historically improved the risk/return profile and provided a higher return per unit of risk than a U.K. investment in isolation.

© The Evidence-Based Investor MMXXIV. All rights reserved. Unauthorised use and/ or duplication of this material without express and written permission is strictly prohibited.